SpaceX Just Bought Cursor for $60 Billion. Why the Deal Matters.

When a rocket company needs an AI coding tool badly enough to spend $60B, the strategic center has moved from model quality to compute access.

Congratulations to the Cursor team! 🎉🥂🎊

Four days after SpaceX’s blockbuster Nasdaq debut at a $1.77 trillion valuation, Elon Musk’s company announced it would acquire Anysphere — the parent company of Cursor — for $60 billion in SpaceX stock. The deal is expected to close in Q3 2026.

Cursor went from a scrappy MIT spinoff in 2022 to $2.6 billion in annualized B2B revenue. Jensen Huang called it his “favorite enterprise AI service”. Patrick Collison said every one of Stripe’s 40,000 engineers is now assisted by it. More than half the Fortune 500 uses it. For a four-year-old company, that is an exceptional outcome, and everyone building AI coding tools — including us — should tip their hat.

The deal also clarifies a shift in AI economics.

Why SpaceX Wants a Code Editor

The strategic value is less about the IDE itself and more about pairing Cursor’s software, data, and distribution with SpaceX’s compute capacity. SpaceX has Colossus — xAI’s 200,000-GPU supercomputer in Memphis, with plans to scale to a million — and needs ways to turn that compute into revenue.

SpaceX lost nearly $5 billion in 2025. Its AI division (xAI, Grok, X) posted a $6.4 billion operating loss in the same year. The company is currently not profitable. It has a mountain of compute capacity and a very expensive rocket program. What it doesn’t have is a distribution channel for AI products that people actually pay for.

Cursor gives SpaceX that distribution channel. $2.6 billion ARR, enterprise contracts with the biggest names in tech, a developer community that loves the product. And Cursor gets what it publicly said it needed: more compute to train its own models. In April, SpaceX secured an option — either acquire for $60 billion or partner for $10 billion. SpaceX chose acquisition over partnership.

The economics increasingly depend on compute + data + distribution. Model architecture still matters, but durable advantage increasingly comes from the surrounding assets.

Model Performance Is Converging

Yesterday we published “You Don’t Have to Use Fable and Mythos to Work on the Frontier” — a post about how the most capable model ever widely available (Claude Fable 5) was pulled by a government directive three days after launch, and how the rest of the field had already caught up enough that production didn’t stop.

The SpaceX-Cursor deal shows the same pattern at the corporate strategy level. It suggests SpaceX sees more durable advantage in distribution and compute access than in model quality alone, because the models themselves are converging.

Look at the numbers from the past two months:

GPT-5.5 hit 82.7% on Terminal-Bench 2.0 at $5/$30 per million tokens

MiniMax M3 scored 59.0% on SWE-Bench Pro at $0.30/$1.20 — 1/40th the cost of Fable 5

Nemotron 3 Ultra holds the top spot among open models on PinchBench with 91% median success

Kimi K2.7 Code (open weights, Modified MIT) hit 62.0 on Kimi Code Bench v2

The gap between frontier closed models and open-weight alternatives is compressing every month. SpaceX appears to be pricing distribution and compute access as the scarcer assets, rather than prioritizing base-model development.

Kimi K2.7 Code’s Benchmark Position

Moonshot AI released Kimi K2.7 Code on June 12 — four days before the SpaceX-Cursor announcement — and its benchmark results show how open-weight models are moving into closed-model territory.

The specs:

1 trillion total parameters, 32B active (Mixture-of-Experts, 384 experts)

256K context window

30% fewer reasoning tokens than K2.6 — directly cheaper to run in agentic loops

Open weights on Hugging Face under Modified MIT

$0.75/$3.50 per million input/output tokens via the Kimi API

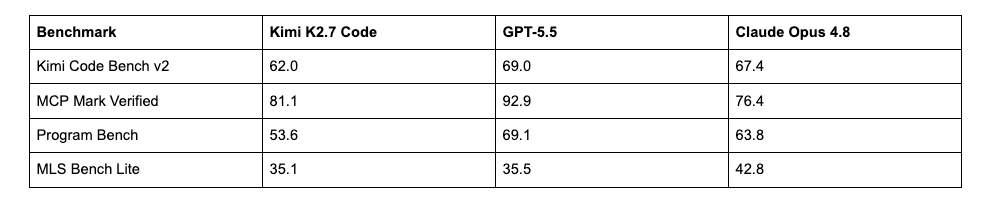

The benchmarks from Moonshot’s own eval table:

K2.7 Code trails GPT-5.5 on most benchmarks while outperforming Claude Opus 4.8 on MCP Mark Verified, which tests tool invocation through MCP, exactly what agentic coding tools need. It is also within striking distance on MLS Bench Lite, at roughly 1/8th the price of GPT-5.5, with weights you can self-host.

The 30% reduction in reasoning tokens is especially relevant for daily agentic use. Every agentic loop that previously burned 1,000 tokens thinking through a code change now burns ~700. Over thousands of iterations per day, the cost difference becomes material.

The Case for Model Freedom Is Stronger

When SpaceX acquires Cursor, Cursor’s model choices stop being purely about what’s best for developers. They become about what’s best for SpaceX’s compute utilization and xAI’s competitive position. This follows from standard acquisition dynamics: product incentives change the day a deal closes.

This is the same dynamic we wrote about when Fable 5 was pulled: depending on a single vendor means your production workflow can change overnight for reasons outside your control.

Kilo’s approach has always been model freedom. Over 500 models in the Kilo Gateway. Full BYOK support. No markup on provider rates. Use Cursor’s models, use OpenAI, use Kimi K2.7 Code, use Nemotron 3 Ultra — use whatever fits the task. Switch when something better arrives. Switch back if a model gets pulled or acquired.

The SpaceX deal doesn’t change anything about Kilo’s architecture. Model-agnostic tools are better positioned to absorb market shifts than tools tied closely to a single provider.

What This Means for Developers

For developers, the implications are practical:

Compute access is becoming a more durable source of advantage. The SpaceX-Cursor deal is a compute play. SpaceX has GPUs. Cursor has distribution. The model layer is increasingly commoditized.

Open-weight models are production-ready. Kimi K2.7 Code, Nemotron 3 Ultra, MiniMax M3 — these models are increasingly viable for production workloads at a fraction of the cost of frontier closed models.

Vendor lock-in has become harder to justify for some teams. Cursor is now owned by a company with broader compute and AI infrastructure incentives, and SpaceX is leasing compute to Anthropic and Google on 90-day termination clauses. The model landscape is moving faster than any single vendor can guarantee stability.

And that vendor lock in - that becomes even more critical as enterprises decide how to deploy AI into their environments. In fact, back in April Gartner wrote about the original SpaceX/Cursor deal as SpaceX’s method of entry into the enterprise. And that type of capture was perhaps best noted as:

Control of the harness steers demand toward preferred models, captures usage at the point of work and creates leverage across the broader developer experience.

That developer experience is something that is critical for leaders and executives to get correct in the age of AI coding. How can you hedge against this risk? Build your workflow around model flexibility. As the market changes, teams that preserve model choice will have more room to adapt.